M&A in 2026: How dealmakers can move faster and reduce risk

Global M&A markets are showing tentative signs of revival. After two years of muted activity, deal values are edging higher, with total deal value reaching approximately $1.94 trillion in the first nine months of 2025, a 10% increase from the same period in 2024.

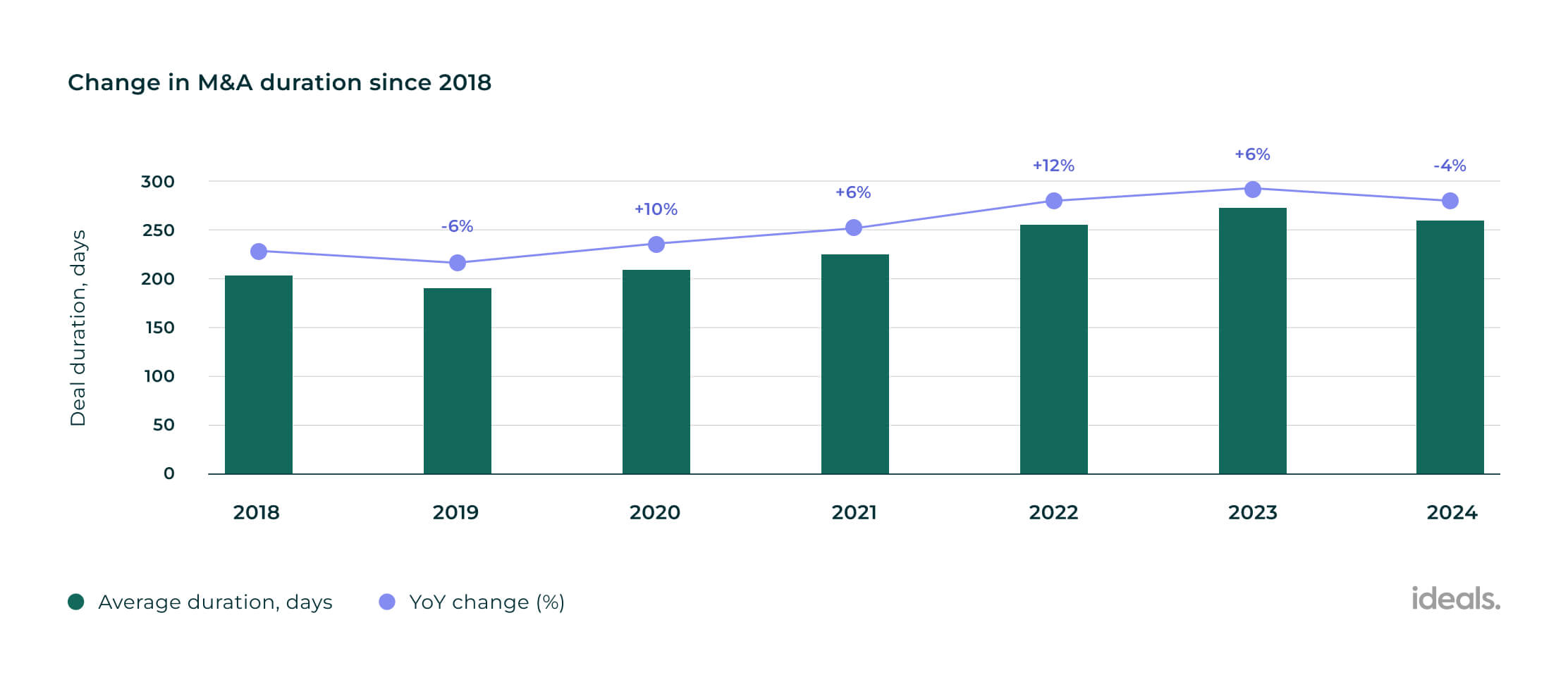

At the same time, transaction timelines are shortening. Our research shows the average time to close a deal fell from 266 days in 2023 to 255 days in 2024, marking the first reduction after four consecutive years of lengthening timelines.

But the recovery remains fragile. Persistent challenges, such as high interest rates, trade tensions and regulatory shifts, continue to temper M&A activity globally. Buyers are scrutinizing margins, supply chains and revenue durability more closely, reflecting increased caution in valuations and deal execution.

Here’s what dealmakers can learn from the recovery so far to help them move faster, manage risk and target the opportunities most likely to succeed.

Caption: Deal timelines were steadily expanding until last year (Source: M&A Deal Trends Report 2025, Ideals)

The path to recovery is uneven

These headwinds have made the market highly selective, with dealmakers carefully choosing which opportunities to pursue. This is reflected in the overall number of transactions, which PwC predicts will fall below 45,000 in 2025, the lowest level in more than a decade.

Meanwhile, deal values are rising, particularly for larger transactions: transactions worth over $1 billion are up 19% year-on-year, and those exceeding $5 billion have risen 16%. Together, these trends indicate a market where headline growth is driven by a relatively small number of high-value deals, even as overall activity remains subdued.

Execution timelines reflect the same dynamic. Larger, more complex deals, involving 50-100 users, took an average of 351 days to complete in 2024, up from 311 days in 2023. Smaller deals, with fewer than 10 users, close more quickly. Across all deal sizes, dealmakers are spending more hours in virtual data rooms and on due diligence, reflecting greater caution and thoroughness in assessing risk and opportunity. This pattern, first documented in 2024, suggests that efficiency gains are balanced by the rigor now applied to every transaction.

“This reflects the complexity of larger transactions, which often involve intricate financial structures, extended valuation negotiations and more comprehensive due diligence,” says Sabine Schilg, VP of Customer Success at Ideals. “Higher-value deals can also face delays as investors may wait for improved conditions amid market uncertainty.”

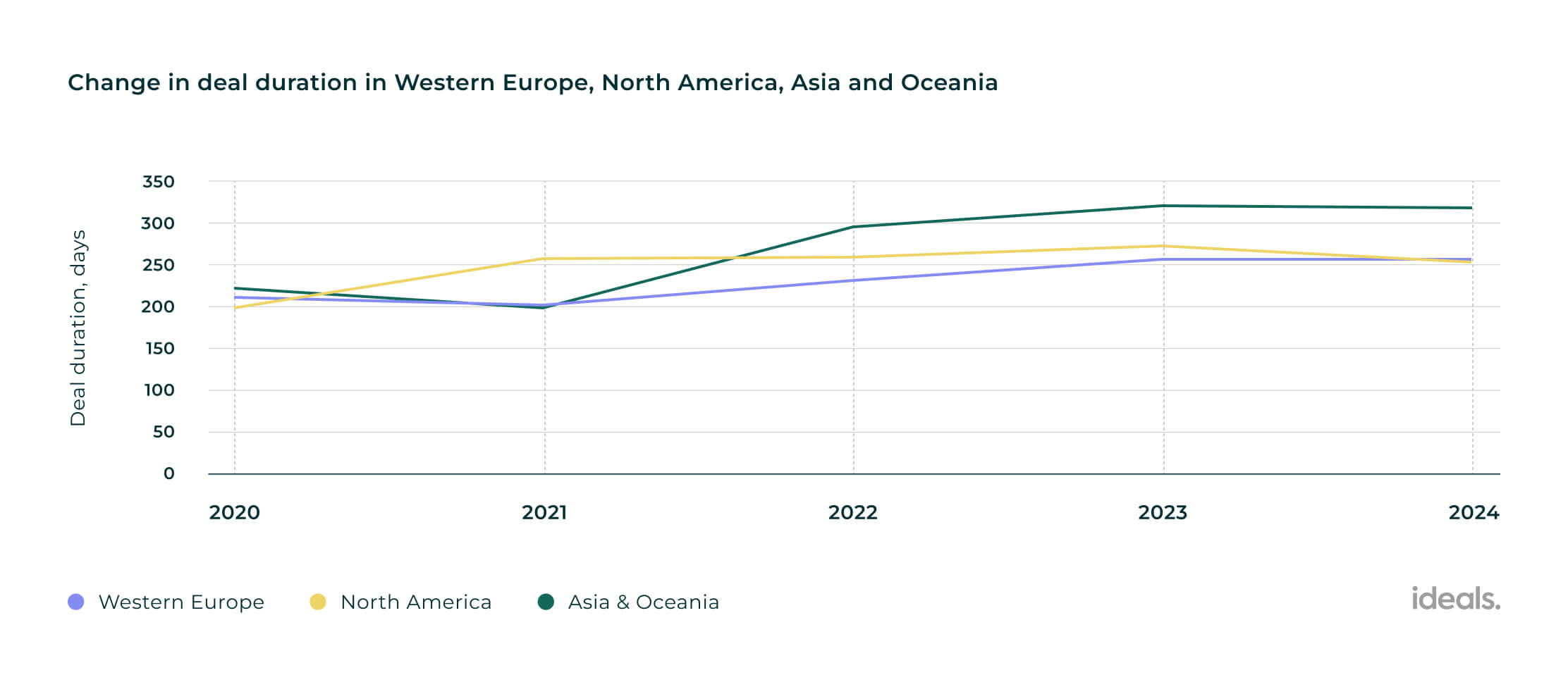

Regional differences shed further light on this uneven recovery. In Western Europe, average deal times held at 255 days, with deal values rising 4%, while North American timelines shortened from 271 to 252 days, with the region accounting for 62% of global M&A value. Asia and Oceania saw a slight dip from 319 to 316 days, supported by procedural changes in China.

Caption: Deal durations vary globally, with efficiency improving slightly in North America (Source: M&A Deal Trends Report 2025, Ideals)

Encouragingly, the outlook for 2026 suggests potential stabilization. Current market assumptions project healthy long‑term returns across asset classes and suggest that, even amid economic uncertainty, disciplined investors adopting diversified strategies (including private equity, real assets and alternatives) will find compelling value.

Credit and capital are a test of discipline

In 2024 and early 2025, financing conditions appeared to stabilize, offering dealmakers a brief window of confidence. Private credit continued to expand its global footprint, increasingly stepping in to fund larger and more complex transactions across North America, Europe and parts of Asia. This has given dealmakers more flexibility and created opportunities for larger transactions.

“While traditional leveraged structures are still in play, we’re seeing more dealmakers turn to private credit for its flexibility and competitive terms,” explains Deven Monga, VP of Sales, North America at Ideals. “With capital access improving, there’s a noticeable uptick in the pursuit of larger transactions, particularly from private equity firms. That’s contributing to more competitive bidding.”

Yet the broader picture remains challenging. In OECD countries, higher borrowing costs are raising refinancing risks for both sovereign and corporate issuers. Interest payments on government debt rose from an average of 3.0 % of GDP in 2023 to 3.3 % in 2024, the highest level since before 2007.

Further adding to the risk, a substantial portion of outstanding debt – both sovereign and corporate – is set to mature within the next few years, creating significant refinancing pressure.

Taken together, these pressures point to a financing environment that is supportive but fragile. Disciplined structuring and early engagement with lenders are becoming as critical as the underlying strategic rationale for the deal.

Geopolitics and regulation constrain activity

Trade uncertainty remains a critical risk to M&A. This year, dealmakers faced renewed geopolitical and policy turbulence, as the reintroduction of tariffs under President Trump’s administration reshaped global trade and added new layers of unpredictability. These measures have complicated valuation models and forced more detailed due diligence.

Meanwhile, the growing regulatory burden adds further friction. Foreign investment review regimes are being expanded globally, with more stringent scrutiny and less predictable checks on national security and mergers.

These concerns have tangible financial implications: higher import costs and retaliatory measures create valuation volatility and distort projections of earnings and cash flow. As a result, buyers are conducting deeper diligence, probing supply-chain vulnerabilities, margin resilience and the durability of revenue streams.

“In good times, deals move faster because competition is fierce, debt markets are flowing, and the focus is on growth indicators,” says David Acharya, Managing Partner at Acharya Capital Partners. “Now, with market volatility and geopolitical concerns, we are digging deeper into financial and operating data, seeking affirmation of continuing financial performance, and heightened downside protection.”

AI continues to cast a halo over tech M&A

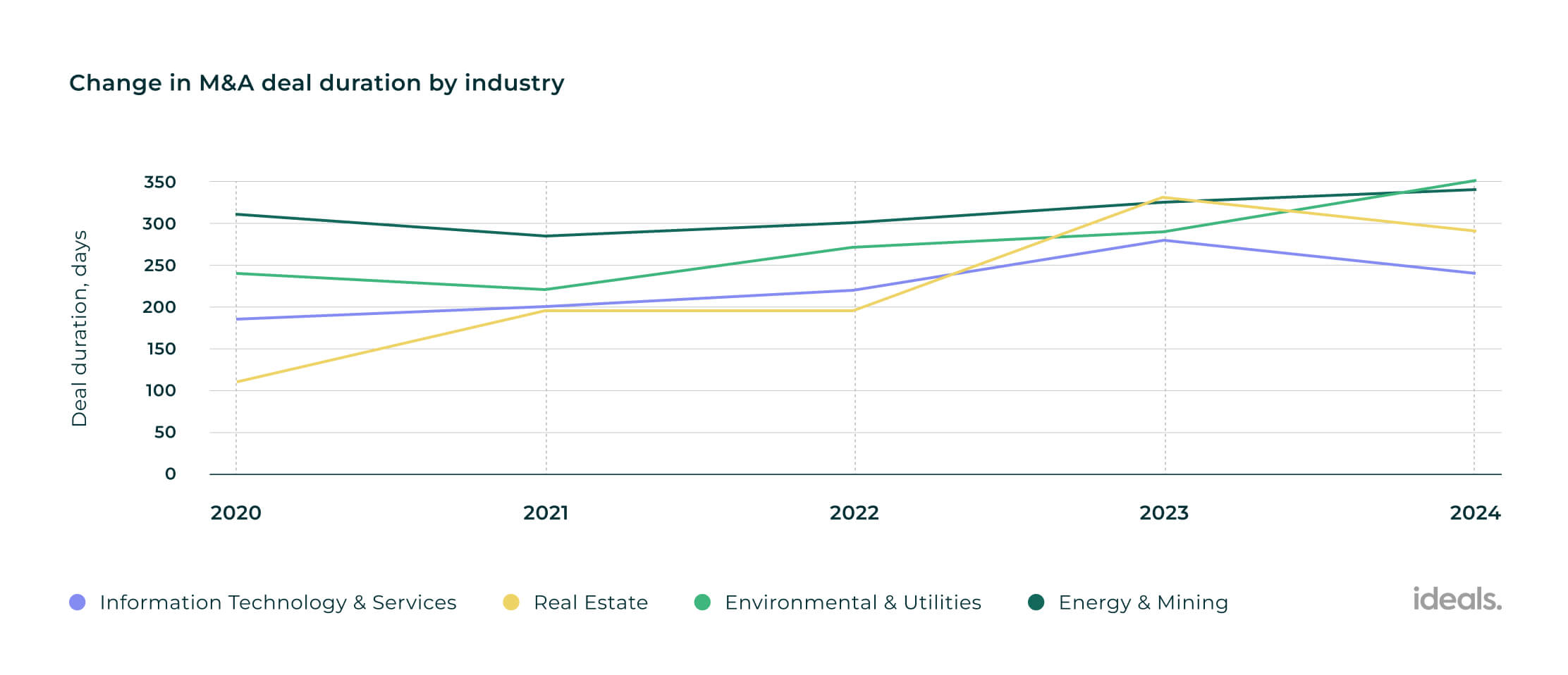

Sectoral divergences are becoming increasingly pronounced. Technology and IT services posted the fastest timelines last year, closing in an average of 244 days — more than 13% faster than the market average. This acceleration is being driven by strong demand for AI infrastructure, which is commanding significant investor attention.

Data from Q3 2025 reinforces this trend: technology dealmaking remained one of the few consistent bright spots in an otherwise mixed M&A landscape, with AI-related transactions boosting both deal value and cross-border activity.

“Data centers, fiber networks and cybersecurity platforms are all seeing increased demand,” explains Chin-Harn Leong, a Partner in KPMG’s TMT Transaction Services. “They’ve become central to the AI-driven investment landscape.”

Meanwhile, heavily regulated sectors such as Environmental & Utilities and Energy & Mining have been facing increasing delays, with deals often exceeding 340 days. This suggests that regulatory complexity can outweigh financing improvements or market confidence in determining deal pace.

Caption: Dealmaking accelerates in Information Technology & Services, and slows in Environmental Utilities and Energy & Mining (Source: M&A Deal Trends Report 2025, Ideals)

AI-driven deals are set to become even more competitive in 2026, with half of all dealmakers now ranking AI and machine learning as a top investment priority. Although this surge reflects genuine strategic demand, some analysts warn that the pace of investment may also be inflating valuations, raising questions about whether parts of the market are entering bubble territory.

Position yourself for M&A success in 2026

If 2025 was a year of cautious recovery, 2026 is a year of opportunity. The modest improvements in deal timelines and financing conditions demonstrate that stabilization is possible. But the recovery remains highly sensitive to external shocks. Rising long-term borrowing costs, renewed trade disputes and geopolitical uncertainty could quickly slow momentum.The winners in the next wave of global M&A will be those who seize these opportunities by investing in technology, strengthening their due diligence processes and anticipating industry and regional complexities. Firms that get this right will not only close deals more efficiently, but also capture long-term value in a highly selective and competitive market.