How to value M&A: Best practices & case studies

Evaluation is integral to M&A success. However, it’s often perceived as one of the most complicated tasks for dealmakers. This article explores the best practices for making M&A evaluations more structured and productive using virtual data rooms. By the end of this article, you will learn about the following:

- Three best practices for M&A evaluations

- Six virtual data room features that aid M&A evaluations

- An overview of comparable company and discounted cash flow (DCF) valuation models with examples

- Key metrics tracked during post-merger evaluations

Three best practices for M&A evaluation

M&A evaluation is the process of reviewing strategic, financial, and risk-related elements of the target company during a merger or acquisition. It is integral to strategic planning, due diligence, and post-merger integration.

Because of the complexity, conducting an M&A valuation can seem overwhelming. However, several practices make this process more effective.

Integrated due diligence

Integrated due diligence (IDD) provides a 360-degree view of the target company. This approach covers not only financial and tax but also operational, strategic, legal, technological, cultural, and operational aspects. Finding interconnected risks within business functions contributes to much more informed M&A evaluations.

Strategic reverse engineering

When it comes to failed mergers and acquisitions, a bad M&A strategy is often to blame. While that is commonly true, the company’s overall corporate strategy can also contribute to its poor M&A choices. When such a strategy contradicts external or internal realities, any perceived strategic fit between acquirer and target company will be inherently wrong.

A better approach to strategic planning would be so-called ‘reverse engineering’, in other words, working back from the end point. A company can ask itself: “What must be true for our strategic choices to work?” The next step is to investigate whether the company’s internal and external conditions meet the required assumptions. This reveals a company’s actual capabilities and you can then build an M&A strategy accordingly.

Virtual data room

Virtual data rooms (VDRs) offer many features to streamline, organize, and effectively supervise M&A evaluations and due diligence. With automation, centralized data, and cybersecurity, VDRs provide the most productive and compliant environment for mergers and acquisitions. Most importantly, migrating your M&A lifecycle to a virtual data room helps reduce a key obstacle in due diligence and M&A evaluations — poor communication.

Six key features of Ideals VDR for M&A evaluation

Ideals virtual data room offers powerful capabilities for evaluating mergers and acquisitions, such as Q&A workflows, drill-down reports, file redaction, OCR (optical character recognition) search, external file sharing, and superior security.

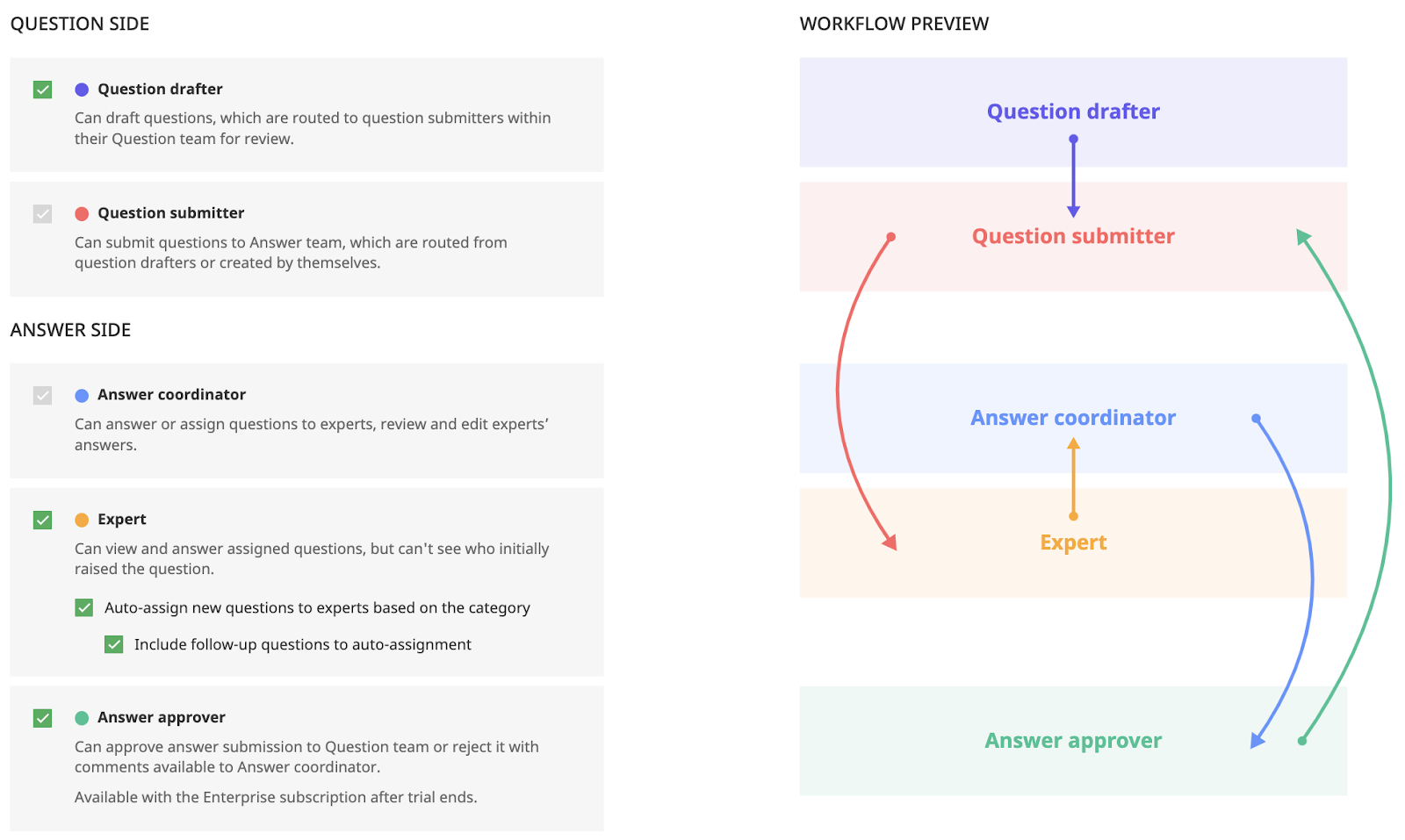

Q&A workflows

Q&A workflows unify and streamline request management, making it more efficient and organized for both the buy-side and sell-side parts of the M&A process. Ideals customers can set up five Q&A roles: question drafter, question submitter, answer coordinator, expert, and answer approver. This feature provides a systemic approach to inquiry management, giving fast access to expertise, reducing email clutter, and improving message control.

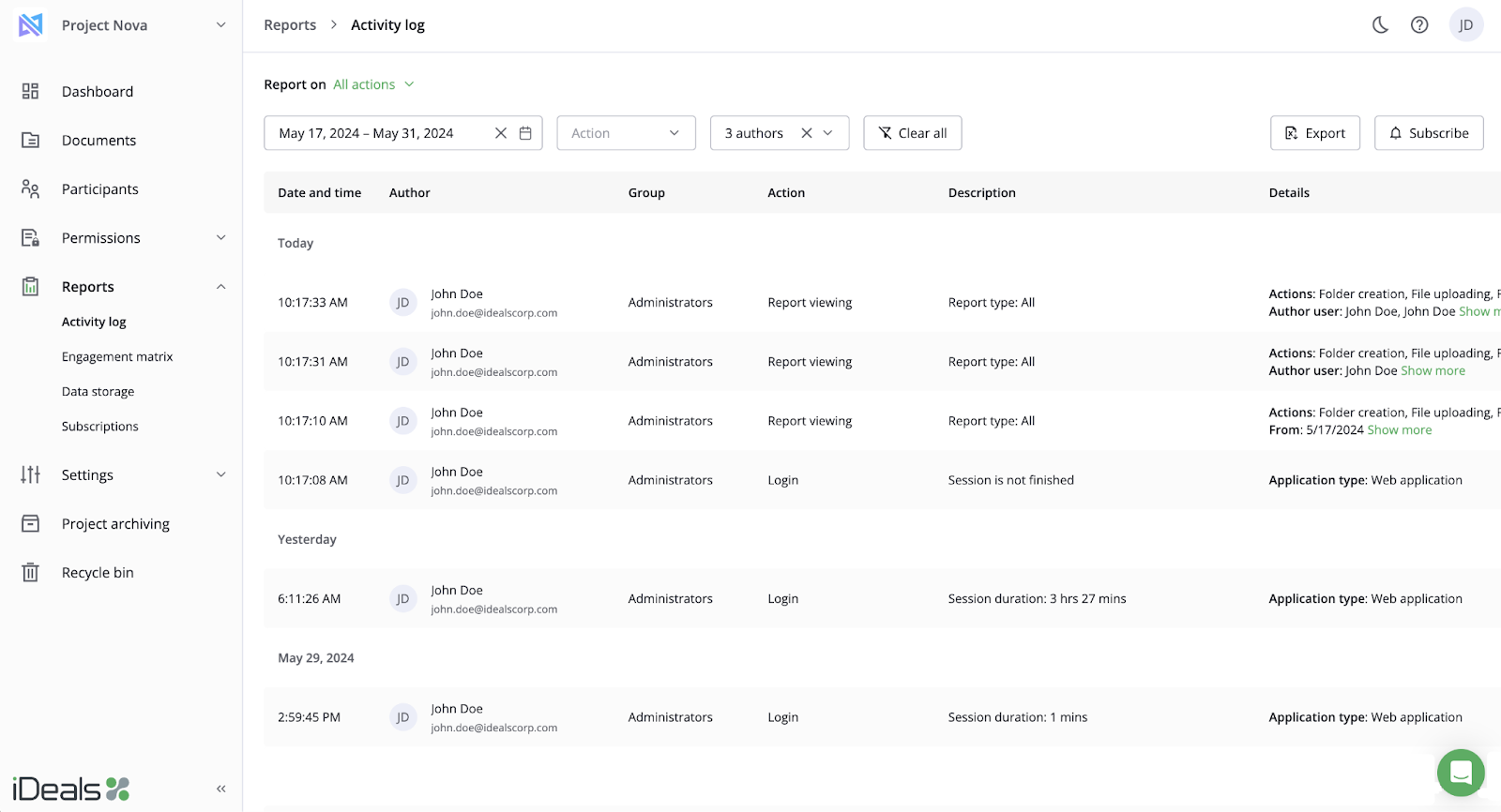

Drill-down reports

Ideals VDR provides an unmatched level of detail and flexibility to M&A reporting processes. Its comprehensive audit trail tracks more than 70 actions over files and folders, groups and users, permissions, reports, settings and more.

Custom reporting parameters are also available. Our team will develop project-specific trackers upon your request, meeting the unique needs of your deal structure.

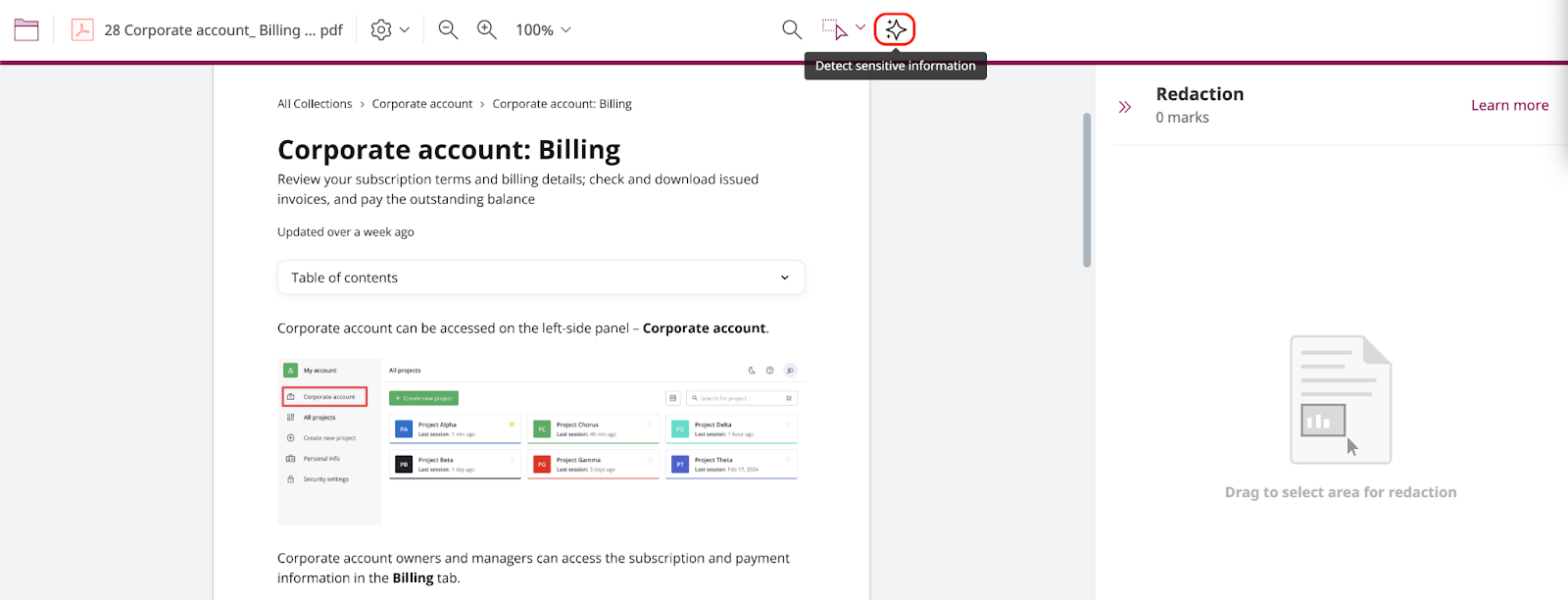

File redaction

Redaction removes sensitive information from files, which is indispensable for sellers as they share large volumes of corporate data. With Ideals’ virtual data room, sell-side dealmakers can quickly remove personally identifiable information (PII) from shared materials to ensure compliance with privacy regulations.

Ideals’ built-in redaction tool supports more than 20 file formats, making it highly versatile for various document types. The process is simple and can be automated to a high degree.

Not only can you apply keyword-based redactions in bulk, but you can also leverage our AI algorithm, detecting various types of sensitive information across the entire document.

OCR search

Optical character recognition converts digitized documents and images into readable, editable, and searchable text formats. This technology helps professionals extract financial data or contractual clauses from unstructured documents, accelerating due diligence evaluations.

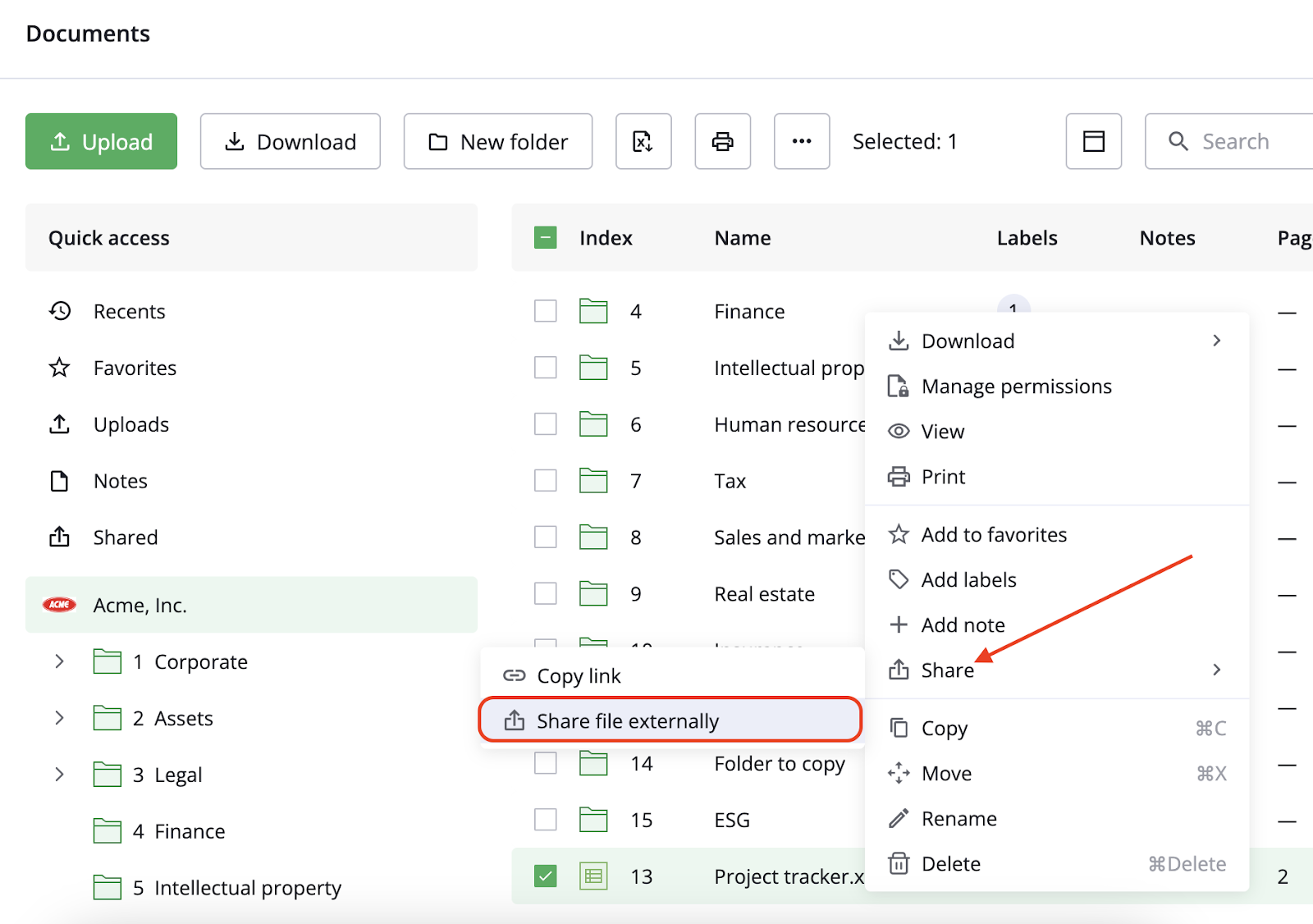

External file sharing

Ideals customers can share Excel and PDF-convertible files with external collaborators while retaining control of the rights and permissions of shared content. Expiration date, domain and email restrictions, watermarks, and download format options can also be configured when sharing secure links. The value of this capability can’t be overstated in M&A evaluations when confidential data must be shared securely and efficiently.

Unmatched security

Our secure M&A data room offers multi-layered protection to all workspace elements, from passwords to individual files on authorized devices. Our top-notch security features are as follows:

| Authentication security | Single-sign-on (SSO) Two-factor authentication Strong password policy Session timeouts Email verification Enforceable NDAs |

| Data & network security | SSL/TLS with 2048-bit RSA data transfer encryption AES 256-bit data encryption at rest IP and domain restrictions |

| Access control & permissions | Eight granular access permissions Information rights management (IRM) encryption Screenshot blocking (Fence View) Secure Spreadsheet Viewer Remote shred and remote wipe User security impersonation Dynamic watermarking |

| Infrastructure security & uptime | 99.95% uptime Disaster and intrusion protection Data center redundancy Real-time data backup |

| Security compliance | SOC 1/2/3, ISO 27001, CCPA, HIPAA, GDPR, PCI DSS, FedRAMP, US/EU Privacy Shield, US-EU DPF |

Case study: Eurallia Finance

Eurallia Finance, one of France’s biggest M&A advisory firms, advises buyers and sellers on M&A valuations and strategic development using Ideals.

Ideals empowers Eurallia Finance to conduct over 50 highly accurate, optimized, and efficient M&A evaluations a year, ranging from €1 million to €30 million in size. Ideals’ Q&A module, audit trails, and document management features streamline Eurallia’s day-to-day activities, particularly due diligence coordination.

Pre-merger evaluation techniques

Some companies are easier to value than others. For asset-rich companies, an asset-based valuation method works well. It’s often enough to subtract liabilities from assets to understand the company’s worth.

For companies where market trends and earnings potential are more important, comparable company and discounted cash flow valuation methods are more applicable. Let’s explore these two methods in detail, starting with the comparable company analysis.

Market-based approach (comparable company analysis)

A market approach (comparable company analysis or CCA) involves estimating the target company’s fair market value based on comparable companies.

This valuation method works well when acquirers have access to a wide range of data when comparing companies (usually public ones due to publicly accessible financial metrics).

The first step is to identify the target company’s business profile. It’s typically done using the following criteria:

- Industry classification (sector, subsector)

- Geography

- Number of employees

- Financing status (VC-backed, startup, LBO, etc)

- Share price

- Market capitalization

- Financials

The next step is to calculate average valuation multiples, such as EV/Revenue, EV/EBITDA, and P/E (price earnings), of similar companies in the same industry. Five to 10 companies are usually enough to derive average values. Afterwards, these multiples are extrapolated on the respective financial metrics of the target company. Let’s explore a few examples.

Example 1: EV/Revenue

Let’s assume the target company’s revenue is $65 million, and the average EV/Revenue multiple of comparable companies is 5.49. To find the target’s EV (enterprise value), one needs to multiply its revenue by the average EV/Revenue multiple of comparable companies. The calculation is as follows: $65 million x 5.49 = $356.85 million.

Example 2: EV/EBITDA

Let’s assume the target company’s EBITDA is $20 million, and the average EV/EBITDA multiple of comparable companies is 15.4. One can find the target’s EV by multiplying its EBITDA by the average EV/EBITDA multiple of comparable companies. The calculation is as follows: $20 million x 15.4 = $308 million.

Example 3: P/E

The average P/E ratio can be used to estimate the equity value of target companies. One can multiply its net income by the average P/E ratio of comparable companies. Let’s assume the target company’s net income is $11 million, and the average P/E ratio of comparable companies is 18. The calculation is as follows: $11 million x 18 = $198 million.

Discounted cash flow analysis

A discounted cash flow (DCF) method estimates the target company’s value (intrinsic value) by projecting its future cash flows. It’s considered more accurate than the CCA method and can be used to understand the future earnings potential of an acquired firm.

DCF is often considered more complex than CCA because it relies on detailed financial data from the target company. The DCF formula is as follows.

Where:

- CF1 is the cash flow for year one

- CF2 is the cash flow for year two

- CFn is the cash flow for any additional year

- r is the discount rate

- n is the year

For this business valuation method to work, an acquiring company needs the following inputs:

Free cash flows (FCF)

Free cash flows can reliably indicate financial health. They can be used to represent expected future cash flows after all expenses.

Discount rate (WACC)

The weighted average cost of capital (WACC) is commonly used as a discount rate in the DCF method. WACC represents accurate expectations of the company’s investors and gives a better understanding of its future performance and expected cash flows.

Terminal growth rate

The terminal growth rate is the rate at which the company’s free cash flows are expected to grow perpetually after the DCF forecast period. The terminal value is calculated assuming the company’s historical growth rate, industry trends and benchmarks, and market conditions. As per conservative estimations, a typical terminal growth rate for mature companies aligns with the 20-year breakeven inflation rate.

Step 1: Calculating discounted cash flows (DCF)

Let’s say Company A wants to buy Company B for $300 million (acquisition cost). To calculate DCFs, Company A uses the following inputs:

- CF1 = $50 million

- CF2 = $54 million

- CF3 = $58.3 million

- CF4 = $62.9 million

- CF5 = $68 million

- r (WACC) = 10%

Company A calculates DCF for years 1-5:

- DCF1 = CF1 ÷ (1 + 0.1)1 = $50 million ÷ 1.1 = $45.45 million

- DCF2 = CF2 ÷ (1 + 0.1)2 = $54 million ÷ 1.21 = $44.62 million

- DCF3 = CF3 ÷ (1 + 0.1)3 = $58.3 million ÷ 1.33 = $43.8 million

- DCF4 = CF4 ÷ (1 + 0.1)4 = $62.9 million ÷ 1.46 = $42.96 million

- DCF5 = CF5 ÷ (1 + 0.1)5 = $68 million ÷ 1.61 = $42.22 million

Now Company A finds the total value of DCF1–DCF5. The calculation is as follows: 45.45 + 44.62 + 43.8 + 42.96 + 42.22 = $218.88 million. This is the present value (PV) of Company B based on discounted future cash flows.

Step 2: Calculating terminal value (TV)

Terminal value (TV) represents the total value of all future cash flows after the forecast period in the DCF method. TV usually accounts for 75% of the present value of the 5-year DCF period. Without accounting for TV, Company B will likely be severely undervalued. TV can be calculated using the perpetual growth formula: TV = CFn × (1+g) ÷ (r-g), where:

- CFn is the cash flow for the last year in the forecast period, which is $68 million

- g is the terminal growth rate, which is 2%

- r is the discount rate, which is 10%

The calculation is as follows: $68 million × (1 + 0.02) ÷ (0.1-0.02) = $867 million.

Step 3: Calculating the total present value (TPV)

First, one finds the present value of the terminal value. Here is the formula: PV of TV = TV ÷ (1 + r)n, where n is the last year in the forecast period, which is five in our case. That is why our formula is as follows: PV of TV = TV ÷ (1 + r)5. The calculation is as follows: $867 million ÷ 1.61 = $538.59 million.

Second, one finds the total present value (TPV) by adding the present value (PV) of discounted cash flows and the present value of the terminal value (PV of TV).

Here is the formula: TPV = PV + PV of TV. The calculation is as follows: $218.88 million + $538.59 million = $757.47 million.

Step 4: Calculating the net present value (NPV)

The final step is to determine the net present value (NPV) of Company B. This can be done by subtracting TPV from the purchase price. The calculation is as follows: $757.47 million − $300 million = $457.47 million.

Step 5: Interpreting the results

If a company’s TPV is positive, the acquisition is potentially profitable, and vice versa. However, for that to be true, all inputs and assumptions must be accurate, reflecting the actual financial health of the assessed company.

The discounted cash flow approach is very sensitive to error and can be highly subjective because it depends on complex projections of a company’s financial performance. Even then, there is no real guarantee that the target company will generate future cash flows as projected. Another downside is that this method doesn’t consider intangible assets, like intellectual property, which may significantly impact the target company’s true value.

Post-merger evaluation: KPI tracking

One of the most critical elements of post-merger integration (PMI) is progress tracking. For this, a dedicated transition team that oversees the integration of the two companies must be established. Otherwise, PMI is likely to go against expectations.

The transition team should develop actionable KPIs to evaluate PMI. Doing so significantly improves the chances of successful integration.

| Integration area | KPI examples |

| Finance | Company’s balance sheet Company’s assets minus liabilities (net asset value) EBITDA margin ROI Revenue Net profit margin Free cash flow Total shareholder returns (TSR) |

| HR | Turnover Satisfaction Engagement Key talent retention Cultural alignment |

| IT | Operational IT cost System consolidation rate Data migration rate Server consolidation rate License consolidation Network uptime Backup & recovery testing time |

| R&D | R&D budget consolidation Project portfolio alignment Technology platforms standardized Knowledge transfer IP portfolio consolidation R&D cost saving |

| Marketing & Sales | Sales growth Customer acquisition cost (CAC) Customer lifetime value (CLV) Customer retention Sales cycle length Churn rate Cross-selling rate Upselling rate |

| After-sales / customer service | First response time First contact resolution rate Resolution time Repeat purchase rate Customer satisfaction score |

| Production & Quality | Overall equipment effectiveness (OEE) Production output Machinery utilization Production cycle time Downtime Quality defect rate First-pass yield Product return rate |

| Procurement | Supplier contract alignment rate Supplier consolidation rate Sourcing lead time Workforce integration rate Budget adherence Supplier terms harmonized |

| Logistics | Warehouse consolidation Inventory turnover Logistics cost reduction On-time delivery rate Transportation cost Inventory record accuracy Order fulfillment time |

Case study: Exxon-Mobil

ExxonMobil’s $81 billion deal is an iconic example of post-merger integration done right. In 1999, Exxon completed a merger with Mobil to achieve cost synergies amidst the oil industry consolidation.

Pre-merger, Exxon anticipated $2.8 billion in business optimization savings. After a year of post-merger integration, however, ExxonMobil managed to achieve $3.8 billion in annual pre-tax savings. This merger created economies of scale and by 2008 reported a record-breaking $45.22 billion net income.

Astonishing synergies were achieved because ExxonMobil established a transition team that oversaw the integration process, tracked KPIs, and proactively addressed hiccups and obstacles.

While KPI tracking was not the only factor in ExxonMobil’s success, it highlights the importance of thorough supervision for successful integration. To this day, ExxonMobil remains an exemplary merger, illustrating how well-executed integration leads to remarkable synergies.

Key takeaways

- The overall best practices for M&A evaluations are integrated due diligence, outcome-driven strategy development, and the use of virtual data rooms.

- The most common methods of valuing a target company are comparable company and discounted cash flow analyses. While both can be valuable, they must also be used cautiously.

- The best way to evaluate a company after a deal is to establish a post-merger integration team to supervise the process using actionable KPIs.

- Embracing effective M&A evaluation strategies and leveraging powerful capabilities of virtual data rooms can significantly boost the transaction’s success.