Top 7 options for M&A financing

Mergers and acquisitions (M&A) is the consolidation of two companies through various types of financial transactions. M&A have numerous advantages — they help businesses expand, acquire new knowledge, move into new markets, and improve their output.

However, along with these benefits and opportunities comes a crucial drawback — a great many expenses for both an acquiring company and a target firm. For example, a standard M&A deal involves lawyers, administrators, and investment banks even before the actual cost of the acquisition has been defined. According to Ernst & Young, M&A transaction costs can range on average from 1% to 4% of the deal value, while the percentage of the M&A expenses also varies depending on the sector the deal takes place.

There’s no doubt about it — mergers and acquisitions are expensive. Therefore, without a lot of cash reserves, companies have to seek out alternative acquisition financing options.

There are a number of different M&A financing options. Choosing the best method will depend on the state of the target company and overall activity in M&A and finance at the time of the transaction.

Read on for an in-depth look at the best available merger and acquisition finance options.

Key takeaways:

- M&A financing is a process through which a deal is funded.

- A buyer and a seller agree on one financing option or a mix of several methods.

- The most common financing options include cash, stock, debt, leveraged buyout, earnout, mezzanine, and third-party financing.

How does M&A funding work?

M&A financing is the process through which companies involved in the deal fund it.

Buy- and sell-side of the deal should thoroughly consider all the available financial mergers and acquisitions options and choose the most appropriate one that will help companies successfully close the deal and undergo the post-closing integration.

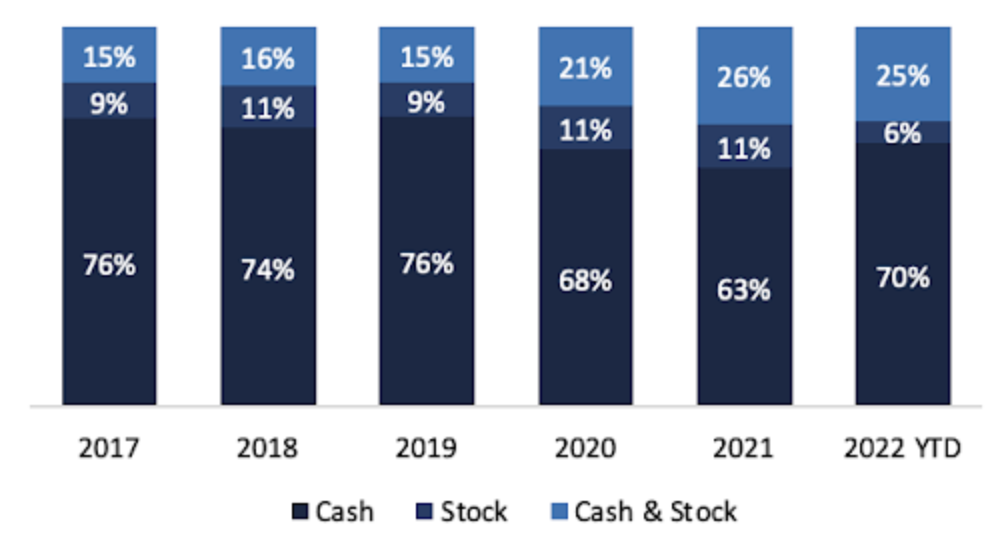

One of the most common sources of M&A financing are cash and stock. The chart below shows the percentage of the deals where stock and cash were in consideration as of 2022.

Source: Crunchbase News

However, it’s not always a single option chosen for M&A funding. Usually, it’s a mix of several options. Moreover, the variety of M&A financing opportunities is not limited to cash and stock. More options are described below.

Top 7 types of mergers and acquisitions finance options

Let’s now define the main 7 types of merger and acquisition finance options, their reasons, advantages, and disadvantages.

1. Exchanging stock

This is probably the most common option when it comes to M&A financing. If one company seeks to merge with or acquire another, it’s safe to assume that the target has a healthy balance sheet with a robust stock offering. In fact, this stock pricing probably led to the M&A activity in the first place.

In a typical stock-exchange transaction, the acquiring company exchanges its shares for the shares of the target company. The offer is communicated directly to the other company’s shareholders.

Financing M&A with stock is beneficial because:

- It’s a relatively safe option as the two businesses share the risks after the transaction, surely guaranteeing more careful management.

- If the buyer’s stock has a higher market value, they receive more of the seller’s company stock shares to account for the difference in market value than if they were paying for their transaction in cash.

- In a merger, shareholders of existing companies will still own an equal value of stock in the single new entity.

However, there is one major drawback to using stock swap as one of the M&A financing methods — stock volatility. No matter how well a company is doing, if word gets out about a possible M&A before any deal has been finalized, there is always a risk of drastic stock price volatility.

The reasons are:

- A company’s shareholders move quickly to sell their stock if they have any reason to feel nervous about the future of a particular company.

- An unannounced or unexplained M&A deal usually raises questions in the financial press. Furthermore, global financial events can wreak havoc on share prices, no matter how well the company is doing.

- Stocks are subject to artificial market movements, such as shorting, although there are regulatory instruments in place to prevent this from having a seriously adverse effect on a company’s value.

While it’s hard to predict what shares will be worth in the future, it’s easy to understand why some companies might be reluctant to exchange stock for stock rather than sell their shares for cash. Often a compromise is reached whereby the sale price includes a mix of shares and cash, reducing risk on both sides and allowing both parties to retain a stake in the new firm.

2. Debt financing

Agreeing to take on the debt owed by a seller is a great alternative to paying in stock or cash. For many target companies, debt is the reason behind a sale, as high-interest rates and poor market conditions can make repaying liabilities nearly impossible.

In these circumstances, the priority for the indebted company is to reduce the risk of further losses as much as possible by entering into an M&A transaction with a company that can guarantee its debts.

Furthermore, being in control of a large quantity of a company’s debt means increased control over management in the event of liquidation, as in this instance, owners of debt have priority over shareholders. This can be another huge incentive for would-be creditors who may wish to restructure the combined company or simply take control of assets such as property or contacts.

However, there are certain drawbacks of such an M&A financing method:

- A company’s debt can reduce its sale value significantly. However, from the creditor’s point of view, acquired assets turn out to be really cheap.

- An acquiring company poses a threat to its assets and even risks potential bankruptcy because in case the new firm fails, the debt must still be repaid.

Of course, it is possible to trade debt in M&A deals without the threat of bankruptcy. Under the terms of the deal, one company may offer to buy up a certain amount of corporate bonds with favorable interest payments, or bonds may be traded between companies as a means of spreading risk and cementing a merger.

If a company’s debts are relatively small, the creditor may simply offer to cover their costs as an extra incentive during the latter stages of the transaction. As with exchanging stock, taking on debt can merely be one part of a complex transaction.

3. Mezzanine financing

Mezzanine capital, also known as stock or subordinated debt, is one method used for M&A financing — it is very similar to financing debt. More specifically, this is a hybrid form of debt and equity financing.

This type of M&A funding is typically chosen by companies that are facing an emergency and need to raise capital quickly. The method is also much more common among mature businesses rather than among startups or young firms.

The major reason companies choose mezzanine financing is a higher rate of return, which can often reach 15-20%. However, there’s a critical disadvantage — it’s riskier in comparison to other ways of M&A financing — but that’s why the payoff is greater. This is because mezzanine funding is unsecured and is subordinate to all other forms of debt.

The return on mezzanine finance comes from five sources:

- Cash interest. The interest rate can be fixed or float based on rates linked to the LIBOR or CRR.

- Payment in kind (PIK). The interest is not paid in cash but with additional debt and gets added to the principal amount and paid on maturity.

- Ownership. It allows mezzanine lenders to convert their debt into equity in the form of a warrant or to ownership in case of default.

- Participation payout. The lender takes a percentage claim on the company’s performance.

- Arrangement fee. Mezzanine lenders charge an arrangement fee, which is paid upfront.

4. Leveraged buyout

A leveraged buyout (LBO) is another mergers and acquisitions finance method where a buyer uses a significant amount of borrowed money to pay for the offered M&A transaction. The ratio is usually around 90% debt to 10% equity.

The main goals of leveraged buyouts are to:

- Let acquiring companies make considerable purchases without having to commit a lot of capital

- Let smaller companies purchase larger, asset-rich targets

- Acquire a competitor

- Privatize a public company

- Improve the underperforming company

An LBO is known to be a particularly hostile takeover and a ruthless way of M&A financing because the target company doesn’t usually sanction the acquisition.

The vast majority of companies suitable for LBOs have substantial operating cash flow, settled and effective product lines, powerful management teams, and well-thought-out exit strategies. Also, private equity firms commonly prefer to buy experienced and reputable companies rather than immature or speculative ones.

5. Earnout

Earnout is a financing mechanism that is often utilized when a buyer wants to acquire a company at a lower price and the seller wants to sell the company at a higher price. In this case, earnout comes as a kind of compromise.

The basis of the earnout financing structure is that only a certain amount of the deal price is paid upfront, while the agreed rest is paid as additional compensation in the future when the business reaches defined metrics.

For example, a company can be acquired for $3 billion plus 5% of gross sales over the next four years.

The main advantages of such an M&A funding method are:

- A buyer has a longer period to pay for the business, rather than doing that upfront.

- If business earnings in future years are not as high as expected, a buyer won’t need to pay as much.

- A seller has an opportunity to spread out taxes over a few years and, this way, reduce the great tax impact on the sale.

However, there are also a few disadvantages:

- It might be a con for a buyer that the seller will probably want to be highly involved in the business for a longer period of time, wanting it to reach the discussed metrics.

- For a seller, there’s no 100% guarantee that the business will bring the expected earnings over the discussed period of time, and this way, the seller won’t get as much from the sale.

6. Third-party financing

As the name suggests, third-party financing implies third-party firms taking part in the deal financing.

These are usually private equity investment companies that can acquire some of the equity of the newly merged company. Through this, they can become involved in certain management decisions.

For the company owners, this can be an advantage and disadvantage at the same time.

On the one hand, company owners might get valuable insights into the company development and growth possibilities from experienced industry professionals. However, letting outside experts into the decision-making process might also become a problem for a company.

7. Cash

One of the primary sources of M&A financing is paying with cash. This method has a number of advantages:

- Cash transactions are instant and mess-free.

- Cash does not require the same kind of complicated management as the stock would.

- The value of cash is far less volatile and does not depend on company performance.

However, there’s a sustainable drawback when financing M&A with cash — multiple currencies. The thing is, exchange rates can vary wildly, as evidenced by the market response to the yen following the Ban of Japan’s deflation program and the British pound following Brexit. Moreover, currency exchange fees add extra expense to multi-national acquisitions.

While cash payment is the preferred method, the price of M&A transactions can run into the millions or even billions, and not many companies have that kind of cash reserves, nor can they access that much cash. However, there are ways of raising or obtaining the needed cash for an upcoming M&A transaction. A few of them are described below.

IPO

An initial public offering (IPO) is when a private company becomes public by offering its shares to public investors.

IPOs can be a good way for a private company to raise money, but upcoming M&A financing is one of the best times to carry one out.

Here’s why:

- The prospect of an approaching M&A can make the investors of the target company more excited about the company’s future, as it signals an ambition to expand.

- IPOs can attract a significant amount of market buzz, so by timing an IPO with an M&A, companies can maximize investor interest and drive up early share prices.

- Increasing the value of an IPO with an upcoming M&A transaction also increases the value of existing shares. In fact, existing shareholders could see their stock value rocket overnight.

However, due to the same volatility that has driven down activity in stock-financed M&A, IPOs can be a risky way of financing ventures. The market can fall just as easily as it can rise, and newly-minted companies are more vulnerable to volatility as they do not have a long track record to reassure investors.

It’s also worth mentioning that sometimes, a private entity uses a publicly listed shell company with no current business operations and limited assets to go public — through a process called a reverse merger. It’s much faster compared to a regular IPO.

Bond issuance

Corporate bonds are a quick and easy way of getting cash for financial mergers and acquisitions, either from existing shareholders or from the public. Companies will typically issue bonds with varying maturity dates — most often ranging from one year to twenty years and a set interest rate (usually less than 5%).

In purchasing these bonds, investors are essentially loaning money to the company with the expectation of receiving a return on their investment. Investors’ profits come in the form of interest payments. However, their actual rate of return will vary according to various market factors, such as the Federal Funds rate set by the Federal Reserve. If the bonds are held to their maturity date, the investor — after having been earning semi-annual interest payments — will receive the face value for the bonds in their portfolio. This makes bonds popular with risk-averse, long-term investors.

Bank loan

Borrowing money can be an expensive affair when undertaking an M&A transaction. Lenders, or owners who have agreed to accept payments over an extended period of time, will demand a reasonable interest rate for the loans they have made.

Even when the interest is relatively small, when dealing with multi-million-dollar M&A financing, the costs can add up. Interest rates, therefore, are an important consideration in funding M&A transactions with debt, and low-interest rates will spike the number of transactions funded with bank loans.

Loan options include re-mortgaging (which is only a viable option if the company has a large property portfolio) and bridge financing.

A bridge loan is a very short-term loan that is intended to “bridge” the gap between expected payments. For instance, a company may be expecting a slew of invoiced payments to come due just after the M&A deadline, which would provide an influx of cash. A bridge loan would cover the shortfall by lending money to a company over a set period of weeks or months.

In a way, this is the payday loan equivalent of the business world and should be approached as a last resort. Interest rates are higher than average, and late payment penalties can be severe. Furthermore, the use of a bridge loan in an M&A transaction may raise concerns with the other party, undermining the deal.

Conclusion

When cash isn’t an option, there are plenty of alternative methods for M&A financing, many of which will result in a speedy and lucrative transaction. The best method will depend on the companies in question, their share situation, debt liabilities, and the total value of their assets. Each method comes with its own risks, hidden transaction fees, and commitments.

However, for most companies, the end result will make it all worthwhile by creating a stronger, more diverse entity that will cover all the initial costs.

FAQ

In short, M&A financing is a process through which the M&A deal is funded. A buyer and the seller agree on a particular financing method or a mix of several financing options.

The M&A deal can be financed both through equity and debt.

There are many financing options for mergers and acquisitions. The most common ones include cash, stock, debt, mezzanine, leveraged buyout, earnout, and third-party financing.