Biotech M&A outlook: Trends, challenges, and opportunities in 2025–2026

The biotech and life sciences sector is emerging from a cautious 2025 and stepping into a new era defined by strategic selectivity. Innovation continues, but the landscape remains challenging. Valuation gaps and evolving regulations are testing market confidence.

This report analyzes how 2026 will shape biotech mergers and acquisitions. It focuses on the rise of consumer-driven health, the integration of AI in research, and private equity’s renewed focus on scalable platforms with clear revenue visibility.

Highlights

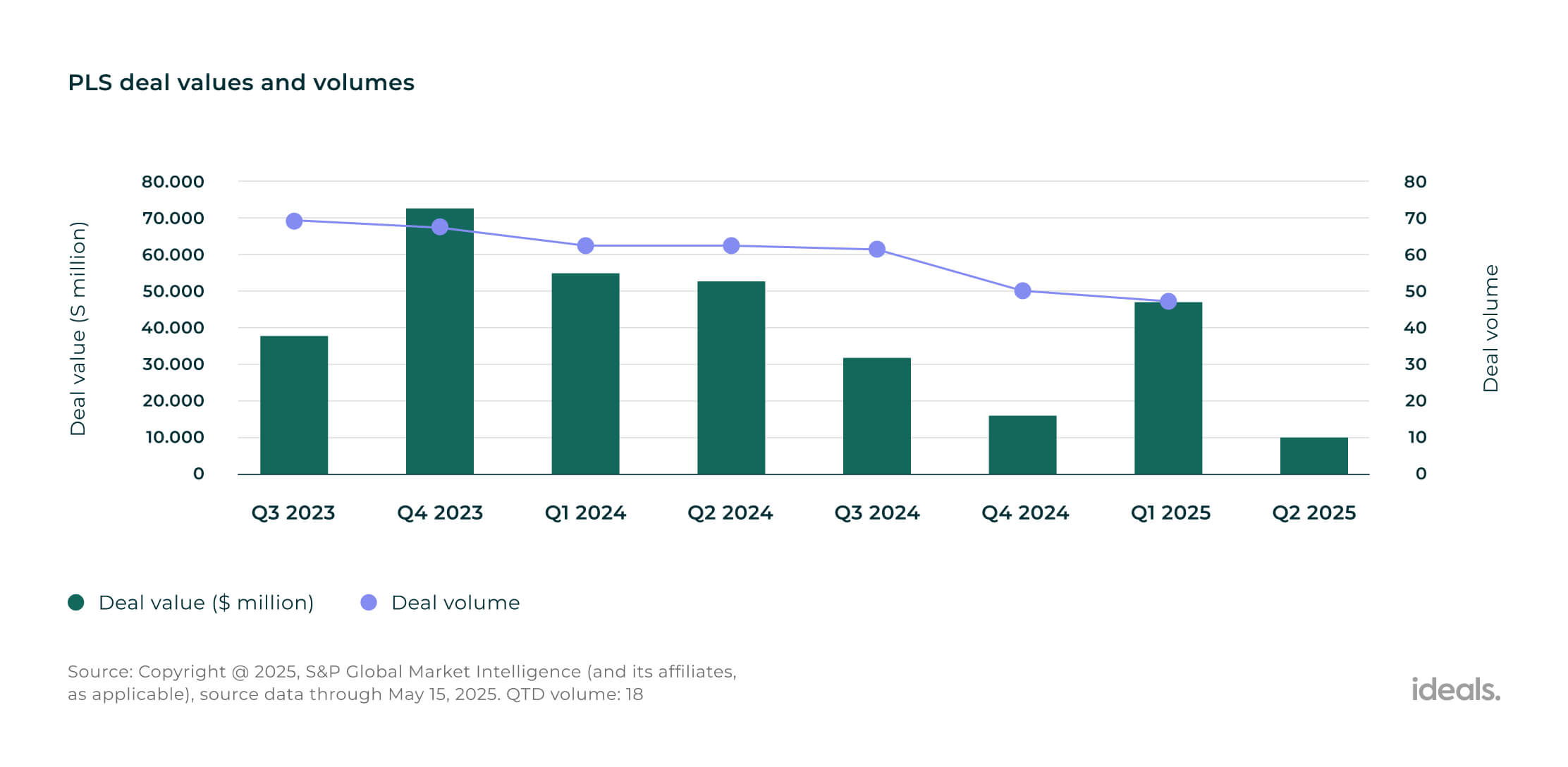

- Borrowing costs remained elevated, and valuation gaps persisted. Overall, biotech M&A activity was muted in 2025.

- Companies favored licensing and partnerships for late-stage assets, while full takeovers lagged.

- Digital capabilities and AI became table stakes; without them, competitiveness slipped.

- Private equity returned cautiously, directing capital toward established, revenue-generating life-sciences firms while early-stage bets saw less interest.

How was biotech investment banking and M&A in 2025?

The biotech and life sciences sector entered 2025 with restrained optimism. Analysts expected dealmaking to rebound as interest rates began to ease, antitrust scrutiny lessened, and therapeutic pipelines remained robust.

At the 2025 J.P. Morgan Healthcare Conference, that optimism translated into approximately $18 billion in announced purchase prices on the first day, led by Johnson & Johnson’s $14.6 billion acquisition of Intra-Cellular Therapies. The deal signaled the company’s intent to secure drugs for the treatment of bipolar depression.

As the year progressed, however, these expectations met a more complicated reality:

- Uncertainty around healthcare pricing reforms, FDA restructuring, and tariff adjustments delayed major decisions and slowed deal closures.

- Biotech funding activity increased, with more companies launching IPOs and secondary stock offerings, but cautious investors contributed to generally weak post-listing performance.

- M&A expansion primarily occurred through smaller, targeted acquisitions that strengthened innovation pipelines rather than through large-scale mergers.

- Companies increased licensing and partnership activity for biologics and late-stage assets, often structuring deals with upfront payments, development or regulatory milestones, commercial milestones, and royalties on future sales.

- Although investor interest in the obesity market remained high, broader expansion was constrained by manufacturing capacity limitations and ongoing pricing negotiations.

- Cross-border partnerships between U.S. and Chinese biotech firms increased, though tighter national-security regulations heightened compliance risks and disrupted supply chains.

Source: PwC’s US Deals 2025 midyear outlook: Pharmaceutical and life sciences

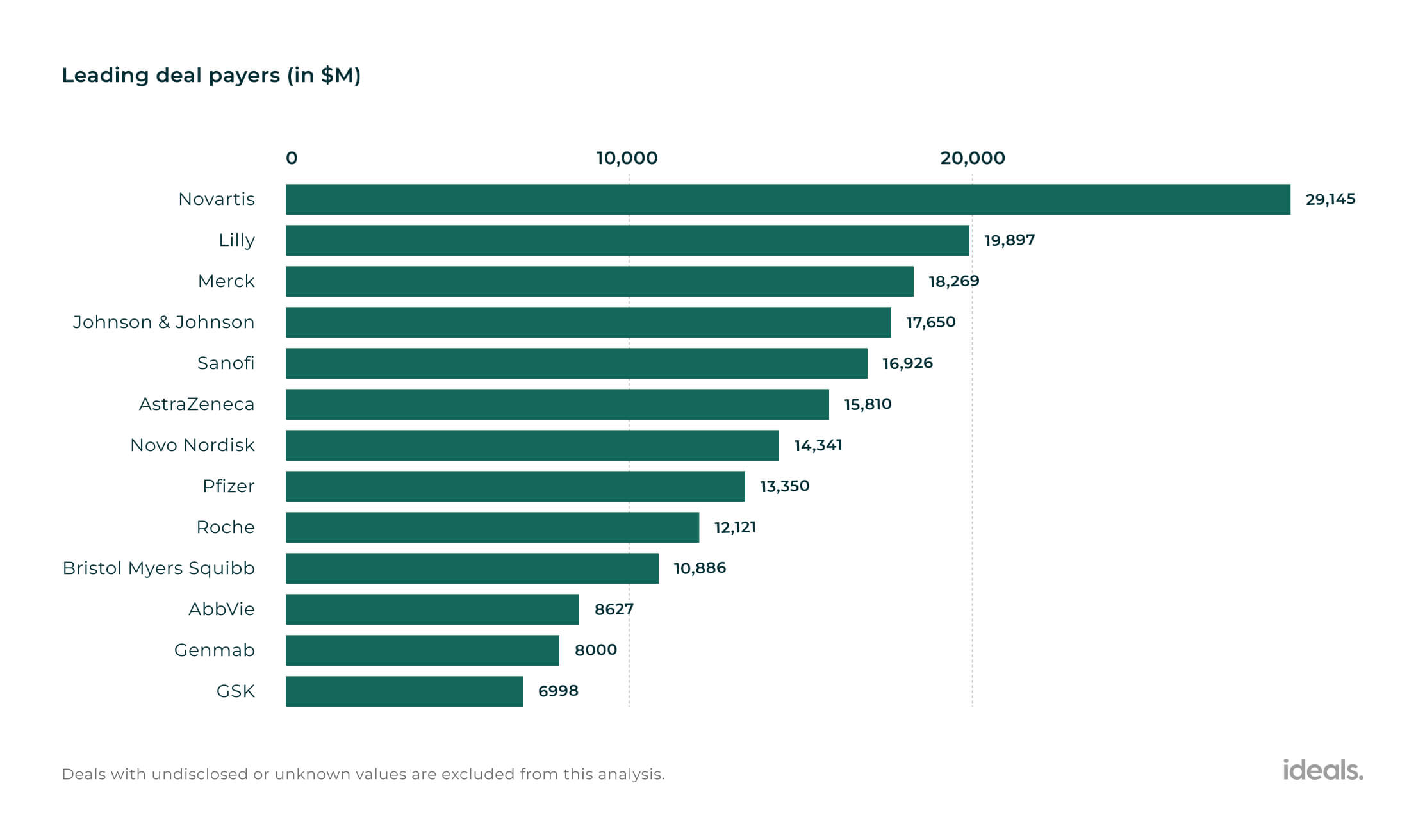

In 2025, a small group of major pharmaceutical players accounted for most deal spending. Novartis led with more than $29 billion in announced acquisitions, while Sanofi, AstraZeneca, and Eli Lilly also made significant moves to bolster their pipelines.

Source: Labiotech

Most deal value is concentrated in oncology and neurology, with small molecules, bispecific antibodies, fusion proteins, and antisense oligonucleotides attracting the most attention from strategic and financial buyers.

Top 10 biotech and life sciences acquisitions

These major deals signal a strategic shift toward pipeline expansion, therapeutic diversification, and disciplined investment in proven, late-stage assets.

| Acquirer | Target | Date | Total deal value | Price per share (+CVR) | Premium | Status |

| Johnson & Johnson | Intra-Cellular Therapies | April 2, 2025 | $14.6 billion | $132.00 | 39% | Completed |

| Novartis | Avidity Biosciences | February 27, 2026 | $12 billion | $72.00 | 46% | Completed |

| Pfizer | Metsera | November 13, 2025 | $10 billion | $86.25 | 3.69% | Completed |

| Merck | Verona Pharma | October 7, 2025 | $10 billion | $107.00 | N/A | Completed |

| Sanofi | Blueprint Medicines | July 18, 2025 | $9.1 billion | $129.00 | N/A | Completed |

| Thermo Fisher Scientific | Clario Holdings | March 24, 2026 | $8.8 billion | N/A | N/A | Completed |

| Roche | 89bio | October 30, 2025 | $3.5 billion | $20.50 | N/A | Completed |

| Merck KGaA | SpringWorks | July 1, 2025 | $3.4 billion | $47.00 | N/A | Completed |

| Eli Lilly | Scorpion Therapeutics’ STX-478 program | March 5, 2025 | $2.5 billion | N/A | N/A | Completed |

| AstraZeneca | EsoBiotec | May 20, 2025 | $1 billion | N/A | N/A | Completed |

Key biotech challenges 2025-2026

The sector generally expects challenging dealmaking conditions in 2026, shaped by financial strain, complex transaction models, and regulatory ambiguity.

Market volatility and financial pressure

The 2025 pharma M&A landscape was characterized by constrained capital markets, limited liquidity, and a widening disconnect between company valuations and asset quality. Many public biotech firms traded below cash, forcing boards to conserve capital and demonstrate clear paths to growth.

This pressure reshaped corporate financial and governance strategies:

- To maintain operational agility, companies cut costs and delayed development milestones.

- Boards actively pursued partnerships with larger companies for co-development or licensing agreements that deliver essential near-term capital.

- Investors increasingly favored businesses with validated clinical data and disciplined capital allocation.

Strategic complexity in creative deal structures

To bridge valuation gaps and manage regulatory risk, biotech firms increasingly turned to inventive deal structures that balance upfront consideration and milestone payments, including contingent value rights (CVR) tied to commercial or regulatory milestones. These models are gaining prominence as mechanisms to unlock value and mitigate risk in a challenging M&A environment:

- Pharma companies are strategically carving out specific drug programs into separate subsidiaries—a “hub-and-spoke” approach that allows targeted asset sales while shielding the core platform from risk.

- Combination mergers, where two capital-constrained biotechs join forces to consolidate pipelines and resources, are also on the rise, creating more viable entities.

- Meanwhile, reverse mergers continue to serve as a practical alternative, offering a faster route to the public markets and clearer exits for investors seeking liquidity.

Regulatory uncertainty and shareholder activism

Uncertainty around Food and Drug Administration (FDA) review processes and broader Department of Health & Human Services (HHS) policy changes, along with shifting trade policies, complicate deal planning and valuations. This environment intensifies pressure on companies from multiple directions:

- Boards face growing shareholder demands for immediate returns, often at odds with long-term strategic goals.

- Activist investors increasingly push for major changes, publicly advocating for mergers, asset sales, or even company break-ups.

- Regulatory delays and unclear guidance prolong due diligence and create new hurdles for cross-border transactions.

2026 outlook for biotech and pharma deals

Biotech M&A activity is expected to increase in 2026, supported by improved financial conditions, evolving regulatory agendas, and ongoing scientific progress.

The analysis below outlines major projections, key market drivers, and the expanding role of private equity in upcoming transactions.

General industry projections

Analysts anticipate a shift across biotech and life sciences in 2026, driven by more proactive consumers, accelerated adoption of digital technology, and a heightened focus on trust and transparency.

Consumer-led transformation reshaping biotech and healthcare

The industry is shifting toward consumer-driven health. Patients increasingly approach healthcare as informed customers, prioritizing transparency, accessibility, and personalization.

This dynamic is pushing organizations to modernize business models and strengthen digital infrastructure. Several key trends will define this transformation:

- Consumers expect health interactions to mirror the seamlessness of digital retail, driving investment in virtual care and direct-to-consumer platforms.

- Trust has become a critical differentiator; companies that build stronger consumer confidence achieve greater loyalty.

- Organizations that fail to deliver convenience, affordability, and clarity will likely lose ground to agile, technology-driven competitors.

Data, digital health, and AI

As data becomes foundational in modern healthcare, organizations must integrate digital systems and artificial intelligence to meet rising expectations for speed and personalization.

For example, a study published on PubMed Central found that “AI-based drug discovery and development could reduce time and cost by 25–50%, depending on the stage and application” Nonetheless, many life sciences firms remain behind in their digital maturity, presenting both risks and opportunities in 2026. The following areas will define where competitive advantages are gained:

- Generative AI is becoming integral to diagnostics, R&D productivity, and personalized treatment.

- Health systems are prioritizing data interoperability to unify consumer records and improve care coordination.

- Boards and executives are adding digital, cybersecurity, and AI expertise to guide innovation responsibly.

Additional reading: Learn how a data room for clinical archiving helps safeguard research data and maintain long-term compliance in life sciences.

Governance and trust as the foundation for long-term growth

Looking ahead, success in biotech and life sciences will depend on balancing innovation with ethical and transparent practices:

- Companies that foster trust and deliver measurable value will secure long-term advantage in an unpredictable market.

- Transparent pricing and open communication about data use will enhance public confidence and regulatory standing.

- Life sciences firms that create educational content and incorporate digital tools to help patients understand and manage their health will strengthen engagement and outcomes.

- Flexible governance structures, such as cross-functional steering committees, will enable faster, data-informed decisions and define resilient organizations in 2026 and beyond.

Biotech M&A market drivers

Several forces are expected to sustain an active M&A landscape. Strategic and financial buyers are positioning to capture innovation as capital conditions ease and regulatory scrutiny becomes less stringent.

The following factors will continue to influence biotech merger and acquisition activity across global markets:

- A major patent cliff, with more than 200 drugs losing exclusivity, is driving pharmaceutical firms to acquire late-stage or market-ready assets to maintain revenue growth.

- Leadership changes at the Federal Trade Commission (FTC) may indicate a more pragmatic merger-enforcement posture, but life sciences deals can still face significant antitrust scrutiny.

- Lower borrowing costs following recent rate cuts are improving access to financing and stimulating buyer engagement.

- Cash-constrained biotechs trading below cash value are increasingly receptive to acquisition or partnership opportunities.

- Rising competition from Chinese biotech alliances and persistent FDA staffing gaps may complicate due diligence and prolong timelines.

Biotech M&A activity is expected to improve selectively in 2026, but large-scale acceleration may remain limited by valuation gaps, cautious buyer sentiment, and market volatility.

“To manage costs and reduce risk, industry players may increasingly favor collaboration and licensing agreements over outright takeovers.” — Nasdaq

Private equity 2026 outlook

As the biotech sector enters 2026, private equity activity is projected to accelerate following a restrained 2025. With interest rates easing and public markets beginning to recover, fund managers are preparing to re-enter the market selectively.

The following trends are expected to shape private equity involvement in life sciences and biotech mergers and acquisitions in 2026:

- Platform biotech acquisition targets are expected to dominate activity as investors pursue “buy and build” strategies around established, revenue-generating life sciences companies.

- Roll-up approaches will broaden to consolidate smaller biotech and medtech firms, particularly those developing AI-driven or digital health solutions.

- Portfolio companies will seek cross-selling opportunities, revenue synergies, and more resilient customer relationships to maintain cash flow during regulatory or market disruptions.

- PE-backed portfolio companies will continue reducing operating costs, including R&D spend where appropriate, to preserve liquidity until valuations rebound.

- Continuation funds will lengthen holding periods, allowing portfolio assets to mature before seeking improved exit opportunities.

“They [PE firms] will likely be less interested in biotech and pharma start-ups still in the early stages of drug development.” BDO USA

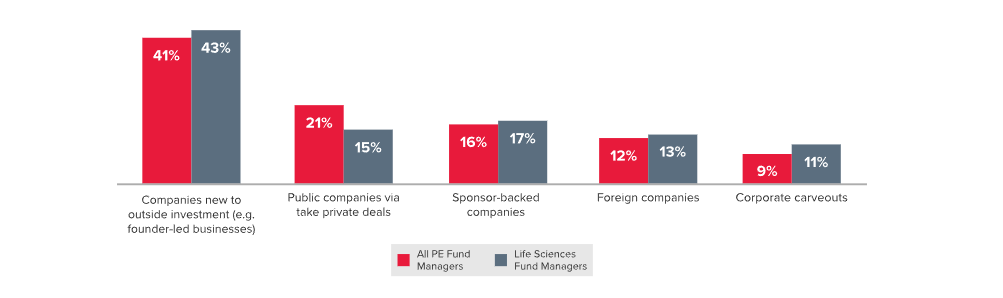

Most attractive asset types for private equity investment in the next 12 months

Source: BDO’s 2026 Outlook on Private Equity Funding in Life Sciences

Biotech companies to watch in 2026

| Company | Therapeutic area | Why watch |

| Ionis Pharmaceuticals (IONS) | Neurology and rare diseases | Several major product launches and filings are anticipated in 2026, including an NDA for zilganersen, positioning Ionis for strong revenue expansion across its late-stage neurological pipeline. |

| CRISPR Therapeutics (CRSP) | Gene editing and cardiovascular health | Early clinical data indicate that its one-time gene-editing therapy can lower LDL cholesterol and triglycerides by about 50%, keeping it at the center of 2026’s leading gene-editing advances and major pharma collaborations. |

| Dyne Therapeutics (DYN) | Neuromuscular and RNA-based therapies | Dyne Therapeutics received FDA Breakthrough Therapy designation for DYNE-251 and anticipates a potential BLA submission for U.S. accelerated approval in early 2026, reflecting accelerating progress in RNA-based treatments for muscle disorders. |

How can Ideals help?

As dealmaking in biotech grows more complex and data-driven, companies need secure collaboration platforms with compliance-related controls to manage transactions effectively. Ideals offers a purpose-built solution for life sciences firms to manage sensitive research data, licensing agreements, clinical trials, and cross-border M&A workflows.

Key ways Ideals supports the sector’s most demanding processes include:

- Secure sharing of confidential data through advanced encryption, granular access controls, and detailed activity logs

- Compliance-related controls and certifications/attestations, including support for HIPAA- and GDPR-regulated workflows, SOC 2/3 reporting, and ISO 27001 certification

- Streamlined due diligence and collaboration among pharma partners, investors, and legal teams through centralized document control and audit-ready reports

- A VDR for clinical trials and regulatory submissions with structured data governance and document version tracking

Discover how the Ideals data room for life sciences helps optimize due diligence and safeguard sensitive data across complex biotech deals.

Bottom line

- Biotech M&A in 2025 focused on smaller, strategic acquisitions as firms balanced innovation with financial caution and regulatory pressure.

- In 2026, dealmaking is likely to remain selective, with moderate growth supported by lower borrowing costs, expiring patents, and private equity participation.

- AI, data interoperability, and consumer-centered models are pushing biotech firms toward greater transparency and faster governance response.

- Organizations that align strategic insight with secure, technology-driven collaboration will be best positioned to navigate a cautious yet opportunity-rich market.